To cash October 1929; back into stocks August 1932. Roughly half the pain of buy-and-hold — not by prediction, but by following confirmed trend breakdown.

When the market broke — and where the strategy stood

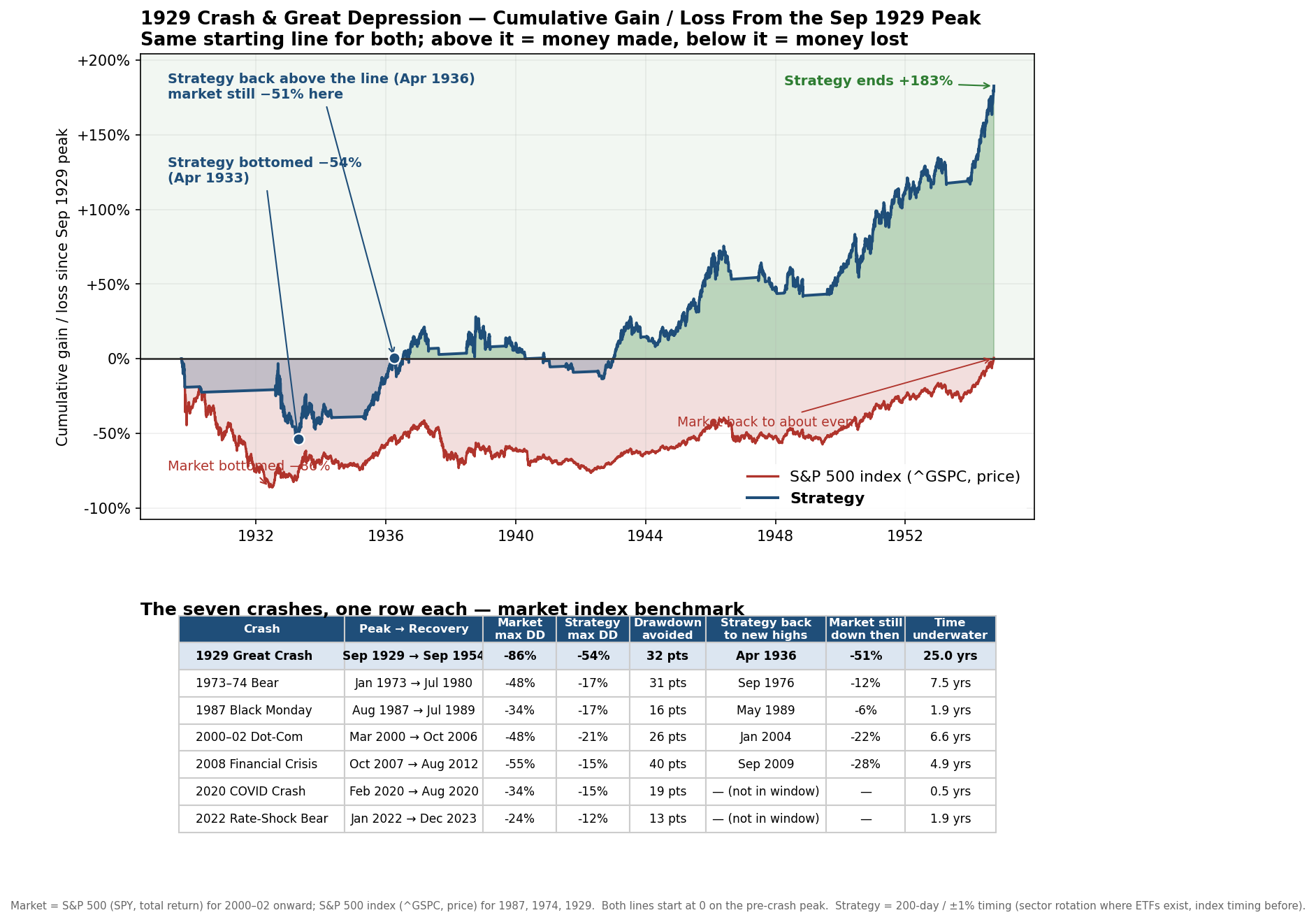

From the peak in September 1929 to the bottom, a plain buy-and-hold investor lost about 86% of their money. It then took until September 1954 — roughly 25 years — just to get back to even. Over that same stretch, the worst our strategy ever fell was about 54%. Roughly half of the pain, for a simple reason: the strategy steps out of the market when the trend turns down, and waits in safe Treasury bills until the trend turns back up.

One thing worth understanding when you look at the chart. The strategy went to cash in October 1929 and did not step back into stocks until August 1932. You might expect its line to lie perfectly flat during that stretch, but it does not. In the 1930s and 1940s Treasury bills paid almost nothing — about 1% a year — so in cash the line stays nearly flat. Once the trend turned back up, the strategy climbed back into stocks and rode the recovery. A rising line during a ‘cash’ period is partly interest earned, and partly the strategy already being back in the market.

Here is the payoff. The strategy climbed back to new highs in April 1936, while the market was still about 51% underwater with years to go. While a buy-and-hold investor was still deep in the hole, the strategy was already making new money.