To cash October 1987; back into stocks June 1988. Roughly half the pain, with T-bills paying 6–7% while the strategy waited.

When the market broke — and where the strategy stood

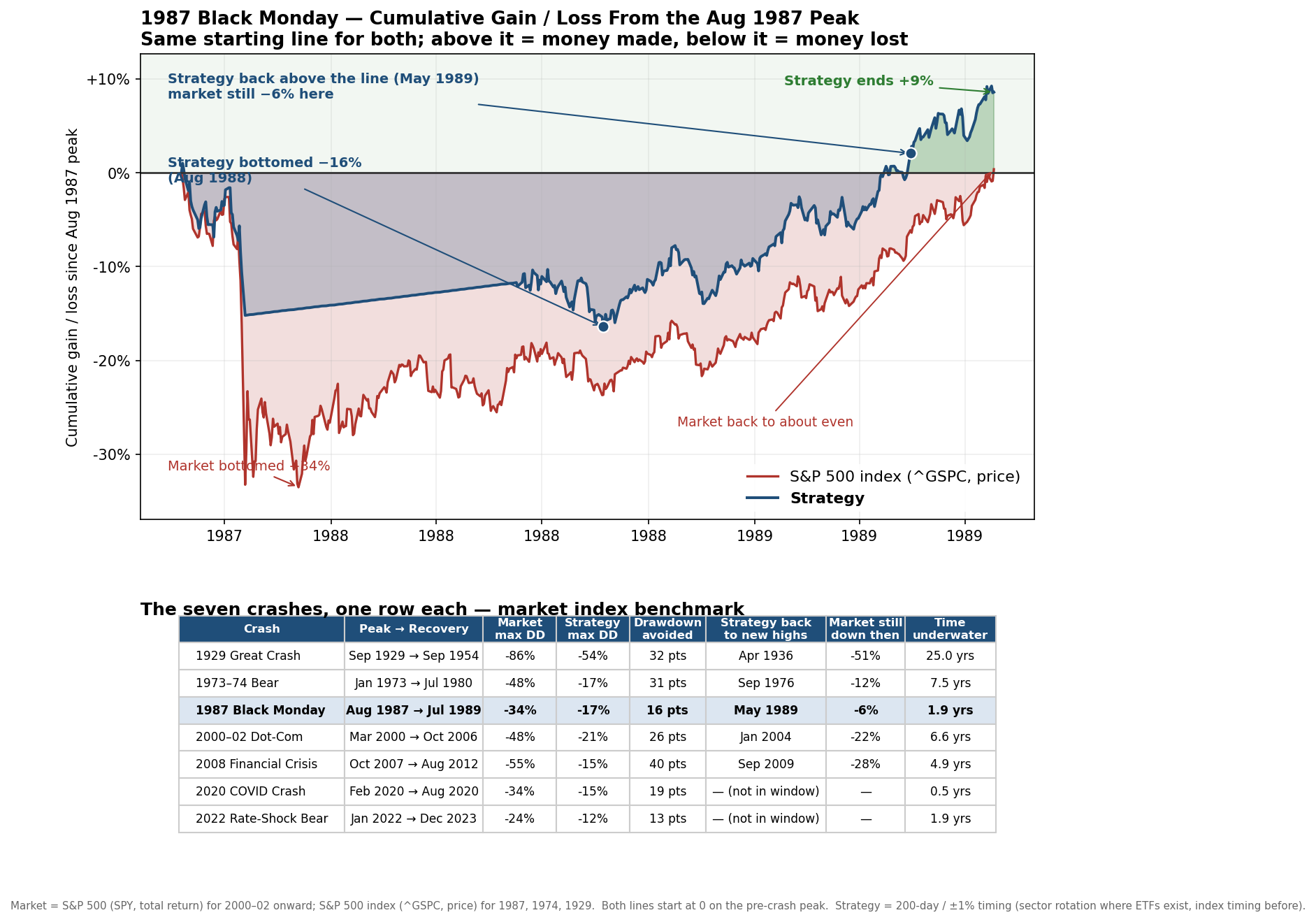

From the peak in August 1987 to the bottom, a plain buy-and-hold investor lost about 34% of their money. It then took until July 1989 — roughly 2 years — just to get back to even. Over that same stretch, the worst our strategy ever fell was about 17%. Roughly half of the pain, for a simple reason: the strategy steps out of the market when the trend turns down, and waits in safe Treasury bills until the trend turns back up.

One thing worth understanding when you look at the chart. The strategy went to cash in October 1987 and did not step back into stocks until June 1988. In the late 1980s, Treasury bills paid around 6 to 7% a year, so even sitting safely in cash the strategy was still earning a nice return, and its line drifts upward rather than lying flat. Once the trend turned back up, the strategy climbed back into stocks and rode the recovery.

Here is the payoff. The strategy climbed back to new highs in May 1989, while the market was still about 6% underwater. While a buy-and-hold investor was still in the hole, the strategy was already making new money.