Every index has to answer one quiet question. When you hold a basket of things, how much of each one do you own? The usual answer is cap weight, which means you own the most of whatever has already grown the largest. The other answer is equal weight, where every piece gets the same size seat regardless of how big it has become. Our strategy uses equal weight, and a reader asked me the fair question. Over the long haul, does it actually pay off, or does it just feel nice?

I went back about a hundred years to find out. Using the Kenneth French industry data from Dartmouth, I compared two portfolios built from the very same forty nine American industries and the very same returns. The only difference was the weighting. One gave every industry an equal seat. The other weighted them by size, the way a normal index does. That way we are measuring the weighting decision by itself, with nothing else muddying the water.

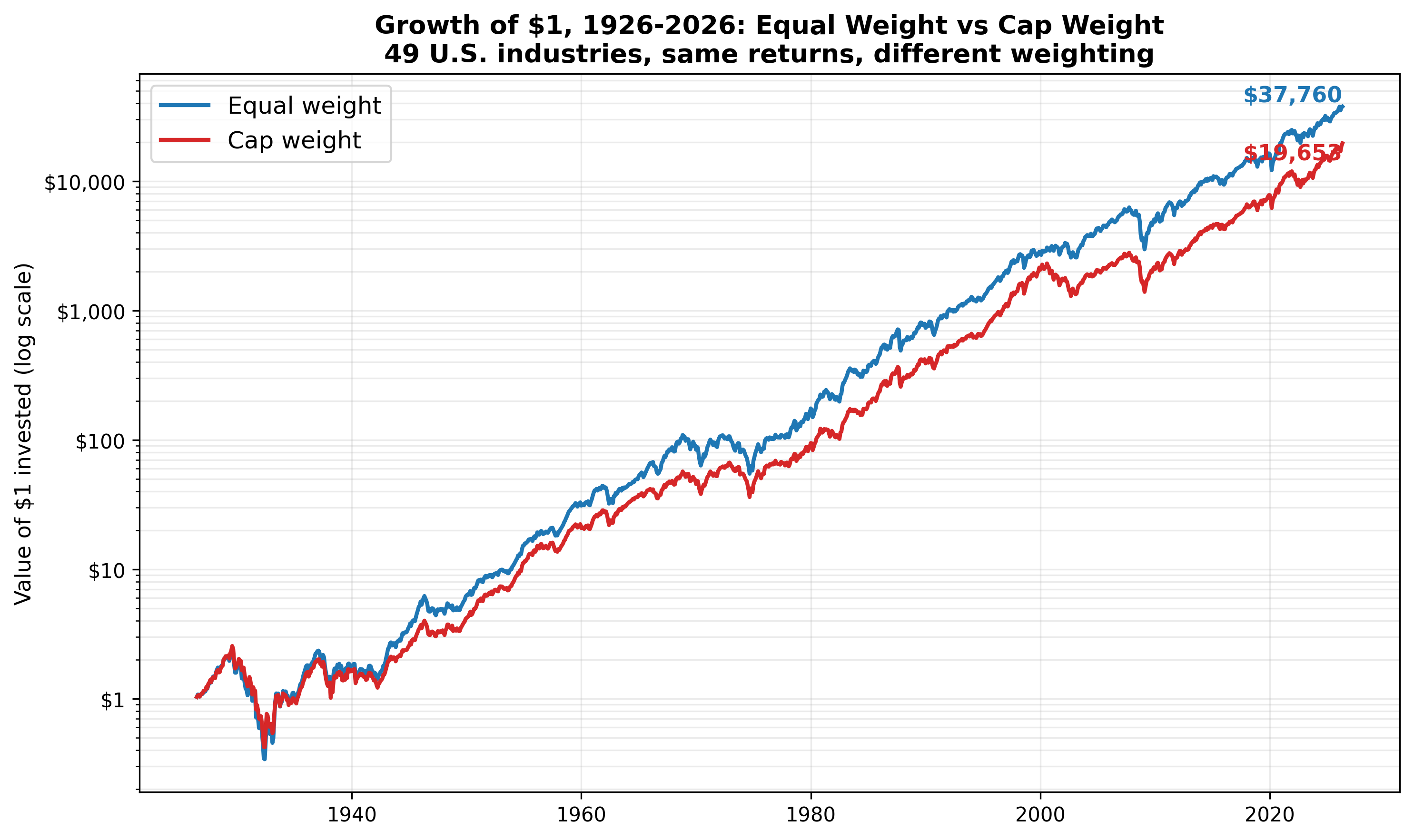

The hundred year scoreboard

Equal weight compounded at about 11.1 percent a year. Cap weight compounded at about 10.4 percent. That gap of seven tenths of a point sounds like a rounding error, but compounding is patient and relentless, and over a full century it becomes enormous. A single dollar invested in 1926 grew to roughly thirty eight thousand dollars under equal weight, against about twenty thousand under cap weight. The equal weight investor ended with nearly double the money, from nothing more than a different answer to that one quiet question.

There is no free lunch here, and I want to be straight about that. Equal weight got its extra return with a bit more bumpiness along the way, because giving the smaller, livelier industries a full seat makes the ride a little rougher. The reward came with a real, if modest, cost in comfort.

It is not luck, it is patience

A century is one long story, so I also chopped the history into overlapping stretches to see how dependable the edge really is. The longer you hold, the more reliable equal weight becomes.

| Holding period | Equal weight won | Avg edge per year |

|---|---|---|

| Any 20-year stretch | 72 of 80 windows (90%) | +1.0 point |

| Any 50-year stretch | 49 of 50 windows (98%) | +0.9 point |

| The last 20 years | Cap weight won | −0.7 point |

| The last 10 years | Cap weight won | −2.1 points |

Read the top two rows slowly, because they are the heart of it. Over any twenty year stretch in the last century, equal weight came out ahead about nine times in ten. Over any fifty year stretch, it won forty nine times out of fifty, and in the single stretch it lost, it lost by a whisker. If your horizon is measured in decades, and for most of us it is, equal weight has been about as close to a sure thing as markets ever offer.

The honest catch, and it is happening right now

Look at the bottom two rows, though, because this is the part I never want to hide. Over the last ten years, cap weight has beaten equal weight by more than two points a year, and over the last twenty it is still ahead. We are living through one of those uncomfortable stretches, and there is a clear reason. A small handful of giant technology companies have grown so large that the size weighted index leans heavily on them, and as long as the giants keep winning, cap weight keeps winning with them.

If that pattern sounds familiar, it should, because it is the same idea underneath everything we do. The market falls in love with its biggest winners, that love makes the cap weighted index more and more concentrated in a few names, and equal weight looks foolish for a while. Then, eventually, leadership rotates, the way it always has, and the patient, evenly spread portfolio gets its turn. The long record says the turn comes. It just does not send a calendar invitation.

The bottom line

Over one year, or even ten, cap weight can absolutely win, and lately it has. Over twenty, fifty, or a hundred years, equal weight has quietly won almost every time, and by enough to matter. Equal weighting is not a clever trade or a market call. It is a long term habit that trades a little comfort now for a better ending later, and it rests on the same belief as the rest of the strategy. No single winner owns the future forever.

— John