For years I have equal weighted the eleven sector funds in the strategy, giving each corner of the market the same size seat at the table. A reader recently asked me a fair question. Why not just let the winners run? If technology has led for a decade, why not simply own more of it?

My honest answer has always been a hunch, so I decided to test it with real numbers. I used the Kenneth French industry data set from Dartmouth, which tracks the returns of forty nine American industries all the way back to 1926. That gives us close to a hundred years of history, not the fifteen year snapshots you usually see in those colorful sector quilt charts online. I want to thank the reader who pushed me, and I want to show you what the data actually says.

The short answer, and the three percent

Leadership does not last. Over long stretches, the industries that had been the biggest winners tended to cool off, and the ones everybody had given up on tended to recover.

Here is the cleanest way I found to say it. Every year I ranked all forty nine industries by how they had done over the previous ten years, from the worst laggards to the hottest winners. Then I watched what each group did over the following ten years. The industries sitting in the bottom fifth, the forgotten ones, went on to earn about twelve and a half percent a year over the next decade. The ones sitting in the top fifth, the darlings everyone loved, earned only about nine percent a year. That gap, a little more than three percentage points every year for ten years, is the whole story in one number. Yesterday’s laggards beat yesterday’s champions, and they did it by about three percent a year.

Making sure the number is honest

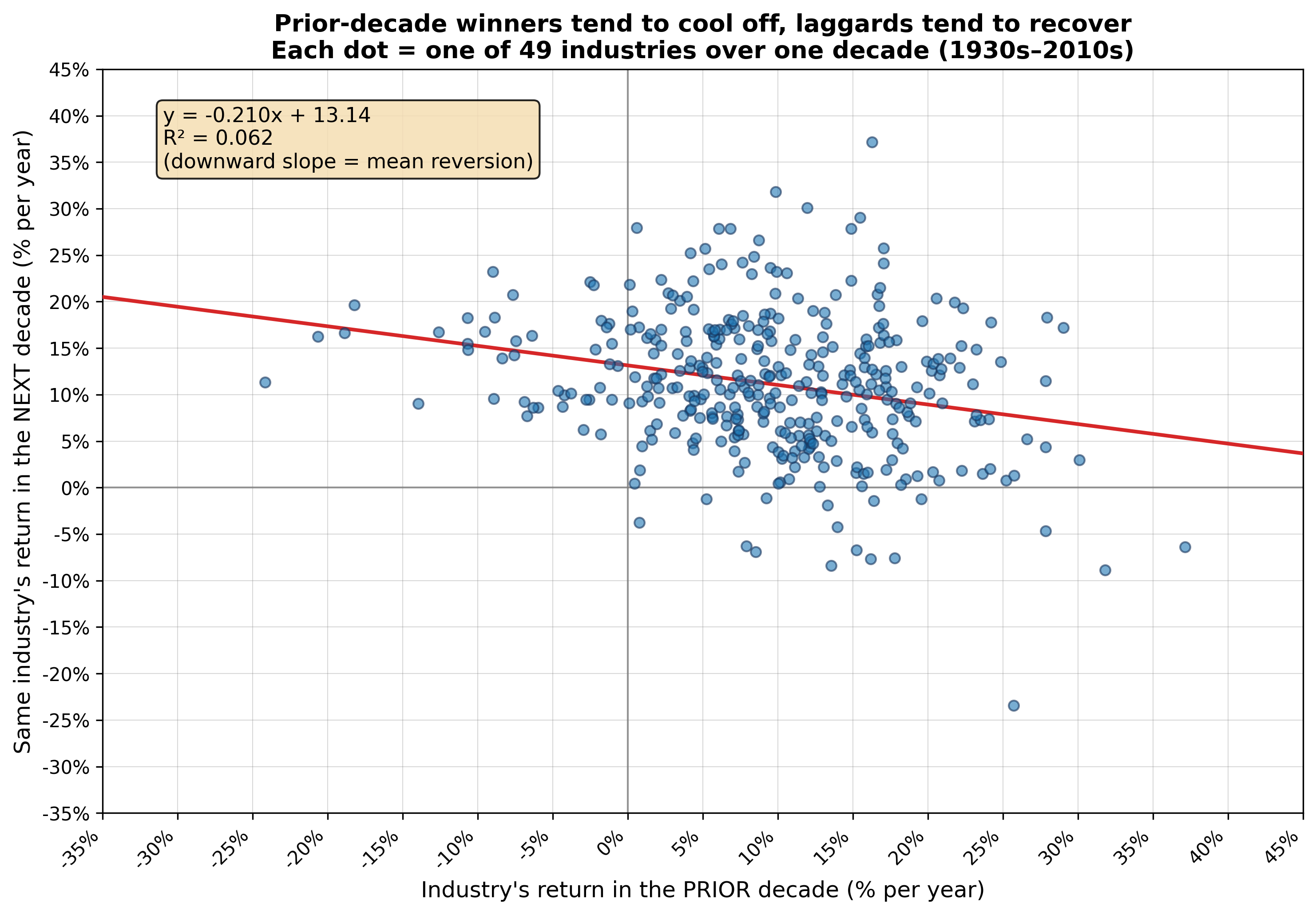

Now, I did not want to fool myself, because that first test has a weakness. When you run it every single year, each ten year window overlaps heavily with the one before it, so those results lean on each other and can look stronger than they really are. So I ran a stricter version that removes the overlap entirely. I simply lined up the clean calendar decades, the 1930s next to the 1940s, the 1940s next to the 1950s, and so on, and asked whether a decade’s leaders faded in the very next decade. Each of those comparisons stands on its own.

The pattern held up. In seven of the eight decade to decade handoffs, the prior winners gave way to the prior laggards. The only exception was the 1980s handing off to the 1990s. When I checked whether that could be luck, the odds came back against it, so this is a real tendency and not a coincidence. The one picture below tells the same story. Each dot is a single industry over a single decade. The horizontal position is how it did that decade, and the vertical position is how it did the next one. The line slopes down, and a downward slope is exactly what mean reversion looks like.

I also checked whether the whole thing hangs on the ten year window, because a result that only works at one length is not much of a result. It does not. When I shortened everything to five years, ranking on the prior five and measuring the next five, the forgotten industries still beat the favorites by about two and three quarters points a year. The one place it falls apart is at very short horizons. Down around three years and shorter, the effect fades and eventually flips, which is simply momentum taking over in the near term. That is exactly why my old monthly test found nothing. Mean reversion here is a slow, patient force measured in half decades, not months.

One example that says it all

If I had to point to a single episode, it would be the technology boom of the 1990s. Software compounded at a remarkable thirty seven percent a year through that decade, chips at nearly thirty two, and computer hardware at almost twenty eight. The internet was real and the excitement was understandable. But the prices had already run far ahead of the businesses, and here is what those same industries did in the decade that followed.

| Industry | 1990s (per yr) | 2000s (per yr) | Swing |

|---|---|---|---|

| Software | +37.1% | −6.4% | −43 pts |

| Chips | +31.8% | −8.9% | −41 pts |

| Hardware | +27.9% | −4.6% | −33 pts |

| Telecom | +17.8% | −7.6% | −25 pts |

The story was true, and the stocks still lost money for ten years, because the crowd had already paid for the story in advance. That is the trap equal weighting is designed to avoid.

The leaders really do rotate

You do not need statistics to feel this. Just look at who led each decade. The parade of names keeps changing, and the crowd favorite of one era is rarely the favorite of the next.

| Decade | Leader | 2nd | 3rd | 4th | 5th |

|---|---|---|---|---|---|

| 1930s | Banks | Aero | Other | Chems | Smoke |

| 1940s | MedEq | Beer | PerSv | Coal | Fun |

| 1950s | Hardware | Chips | Toys | LabEq | ElcEq |

| 1960s | MedEq | Hardware | Other | Coal | Hshld |

| 1970s | Defense | Gold | Coal | Oil | Aircraft |

| 1980s | Tobacco | Beer | Food | Textiles | Telecom |

| 1990s | Software | Chips | Hardware | ElcEq | Finance |

| 2000s | Coal | Tobacco | Mines | Defense | Agric |

| 2010s | Entertain. | Defense | Ships | LabEq | Chips |

Hard assets and energy in the 1970s. Steady consumer names in the 1980s. Technology in the 1990s. Coal, tobacco and mining in the 2000s. Then technology again in the 2010s. Energy is the clearest round trip of all, leading in the 1970s, trailing in the 1980s, leading again in the 2000s, and trailing again in the 2010s.

What this means for how we invest

I want to be careful here, because this is not a trading signal. It is far too slow and too noisy to tell you what to buy this month or even this year, and when I collapsed the forty nine industries down into the eleven broad sectors we actually trade, the tendency was still there but gentler and harder to prove, simply because eleven baskets is a lot less to work with than forty nine. So I am not asking you to go buy whatever has lagged.

What the century of history does support is the quiet discipline behind equal weighting. We are not trying to guess which sector will own the next ten years, because history says nobody owns it for long. By giving each sector the same starting weight, we keep from letting yesterday’s champion quietly grow into tomorrow’s oversized risk. Think of it less as a bet and more as humility. No corner of the market gets to become the whole portfolio just because it has been winning.

The honest bottom line

Sector leadership is sticky in the short run and unstable in the long run. Chasing last month’s winner is a fool’s errand, but assuming this decade’s champion will also win the next one is its own kind of mistake. Equal weighting across sectors is my way of respecting that uncertainty. It is not a prediction. It is a refusal to let the market’s current favorite become my single largest worry.

— John