Picture a subscriber who retires in October 2007 with $200,000 and starts drawing $666.67 a month. That is the classic 4 percent rule: $8,000 a year to start, with the check growing alongside the cost of living. And grow it does. By early 2009 the monthly draw is about $677, and by the tenth year it has reached $785. Over the full decade this retiree takes out $87,385, month in and month out, through everything that follows. That schedule never pauses, and that is the whole problem: a retiree cannot wait out a bear market the way a saver can. The bills arrive whether the market has recovered or not.

Into the storm

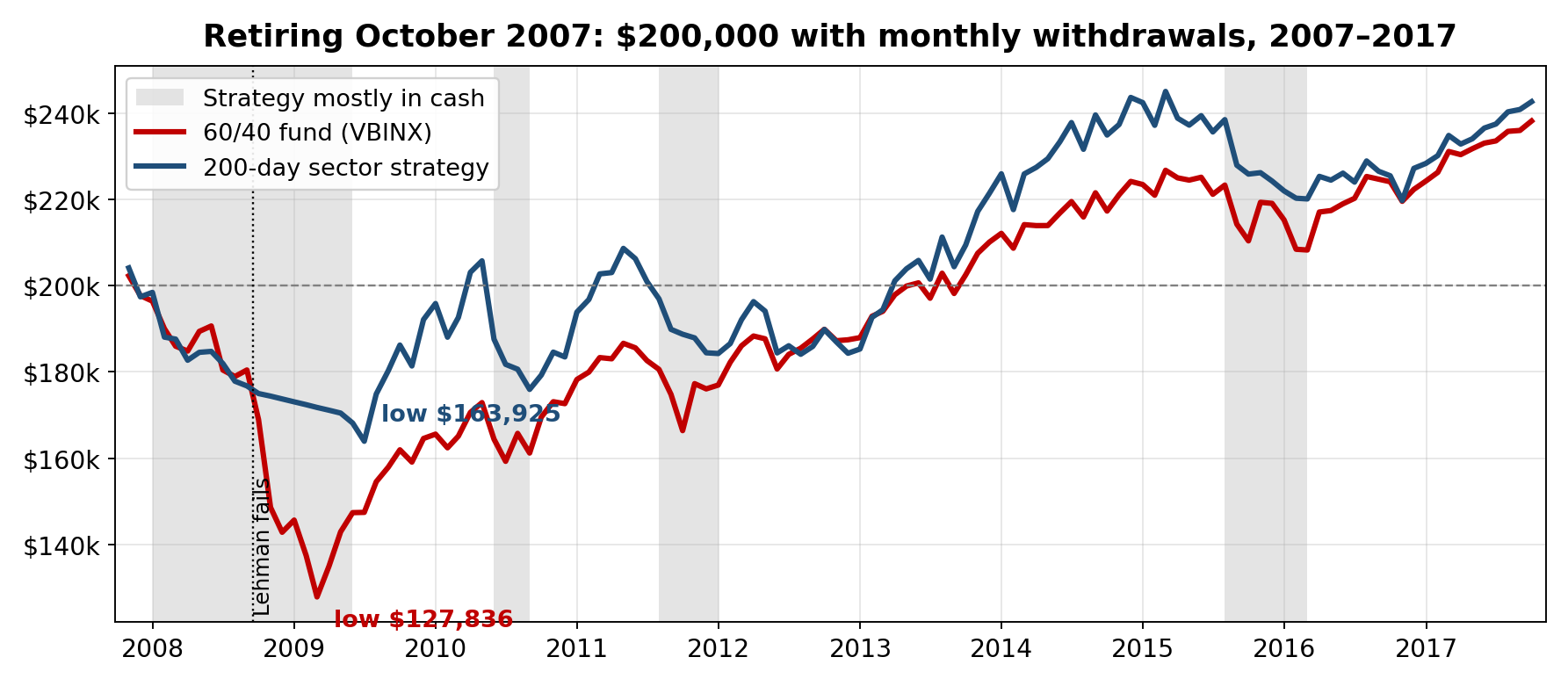

What followed was the worst financial storm since the Great Depression. From late 2007 to March 2009 the stock market fell about 55 percent. I mention that number not as a benchmark but as a measure of the fear in the air: banks were failing and perfectly sensible people stopped opening their account statements. Every dollar this retiree sold in those months was sold to pay real bills, at whatever price panic was offering that day.

What the rule actually did

Here is what the 200-day sector strategy actually did. As sectors fell below their long-term trend lines it moved them to cash a piece at a time, starting in November 2007. By June 2008 it held just one sector in nine, three months before Lehman Brothers failed. At the March 2009 bottom it held none at all. On the day the market touched its low, this retiree had $171,114 sitting mostly in cash, while the same retiree in a standard 60/40 fund had $134,979 and falling. That difference of about $36,000 arrived at exactly the moment when fear makes people do permanent damage, like selling everything and never coming back.

I want to be honest about what cash did and did not do. The account still drifted down during the crisis, touching its own low of $163,925, for two simple reasons. The withdrawals never stopped, and by late 2008 cash paid essentially nothing, so the account shrank by the size of each check. And a trend rule cannot step aside until prices have already broken the trend, so the strategy absorbed the first slice of the decline before it got out. Protection here means a scratch instead of a wound: the strategy lost about 13 percent through the crisis while the 60/40 fund lost about 21 percent and the stock market lost more than half.

Getting back in

Then came the half of the story people forget: getting back in. Nobody felt brave in the summer of 2009. The economy was still shedding jobs and the headlines were still awful. But as sectors climbed back above their trend lines the rule bought them back, one by one, beginning that June, and by December 2009 the strategy was fully invested and rode the recovery all the way up. That is the quiet advantage of a rule: it does not need nerve, and it does not need the news to feel better first.

The final score

The final score after ten years: the strategy retiree finished with $242,634, the 60/40 retiree with $238,163, both after drawing out that same $87,385. The account paid a decade of rising income and still ended $42,634 larger than it began. That is the arithmetic of retirement: it is not the average return that ruins people, it is being forced to sell, month after month, into a deep bear market that arrives early. The strategy gives up roughly 1 to 1.5 percent a year in the long run. I think of that as an insurance premium, and a fairly priced one. Remember too that you are not paying an investment adviser on this portion of your portfolio, and with advisory fees commonly running about 1 percent a year, that savings covers most of the premium by itself. You do not buy homeowner’s insurance hoping to come out ahead. You buy it for the one night there is a fire, and nobody gets to choose which decade they retire into.

— John